Banks Offer More Than Fintechs…With The Right Partner

Small and medium-sized businesses have always been the growth engine in our economy and the mainstay of successful commercial banks.

As technology becomes easier to access for your business customers, your bank faces competition from both traditional players and new entrants. Larger banks are growing, in part by acquiring smaller banks, creating mega-organizations with the extensive resources they need to develop and offer new products and services. At the same time, Fintechs are entering the banking space, offering person-to-person payments, small business lending, insurance, Buy Now Pay Later (BNPL) and other services that customers are searching for and connecting with in increasing numbers.

Given all this competition and clutter for mind share, how can your bank stand out? One place to focus is any service which helps your small business customer better manage cash flow. Banks have traditionally always had the advantage and delivered results for their business customers. At the core of managing cash flow, small businesses need easy-to-integrate and manage billing, payment processing, accounts receivable management and collections services.

A payment gateway is one of the essential services when it comes to managing cash flow. From generating invoices, processing credit card, ACH and alternative payments, and automatically reconciling payments received to open invoices and bank deposits, many of your business customers rely on a payment gateway. That includes payments made in-store, online, in-app as well as subscription and recurring payments. The entire revenue and accounts receivable side of your customer’s business is managed through their payment gateway provider.

Is your bank already offering payment gateway services? If not or if you are looking for alternatives, the options typically are either (i) work with a processor (Fiserv, FIS) or (ii) partner with a technology company (Stripe, Square, Paypal, Exact Payments). Of course, a number of technology companies now actively compete with banks. For example, both Stripe and Square offer a full suite of small business lending programs.

Whichever partner path you consider, here is a short list of important criteria you may want to assess in the evaluation process (in order of importance to your business customers):

- Clear technical documentation and tools which enable integration in days rather than weeks.

- 100% reliability and scalability. Always available and scalable as the business grows.

- Highly responsive technical support 24 x 7 (ask for customer references)

- Comprehensive data security program including card tokenization. PCI Level 1 certified service provider is a must.

- All major payment types including multicurrency support

- Value-added services which (i) increase approval rates; (ii) improve security or (iii) lower cost of payments. Examples include: 3-D Secure 2.0, Network Tokenization and Realtime Card Account Updater

Your bank provides a range of critical services to growing businesses in your market. With the right gateway partner, you can continue to provide the personalized service you are known for as well as offering payment capabilities that your customers need to compete.

To learn more, Bank Partners – Exact Payments.

TOP POSTS

Thought Leadership, Whitepapers

How to choose an integrated payment model for your software platform

Infographics, Thought Leadership

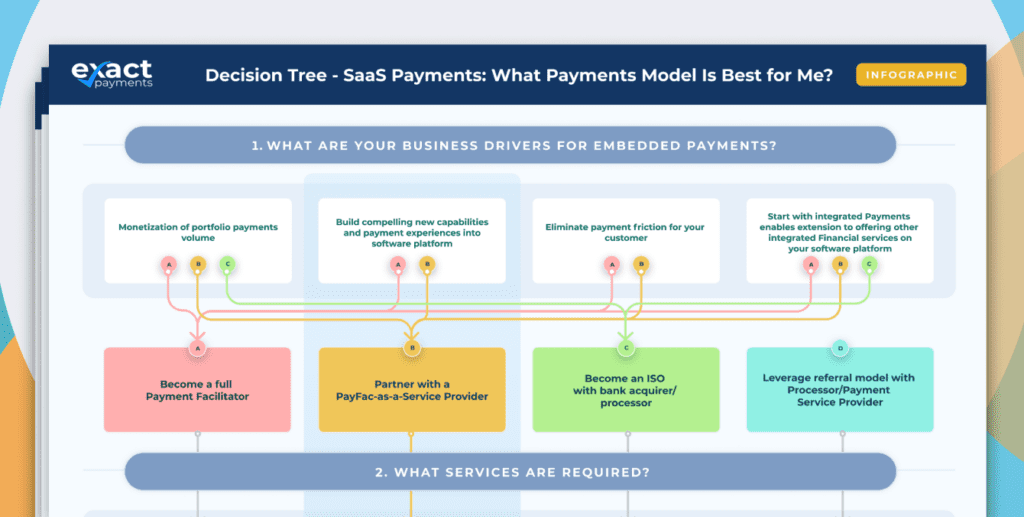

Decision Tree – SaaS Payments: What is the Best Embedded Payments Model for Me?